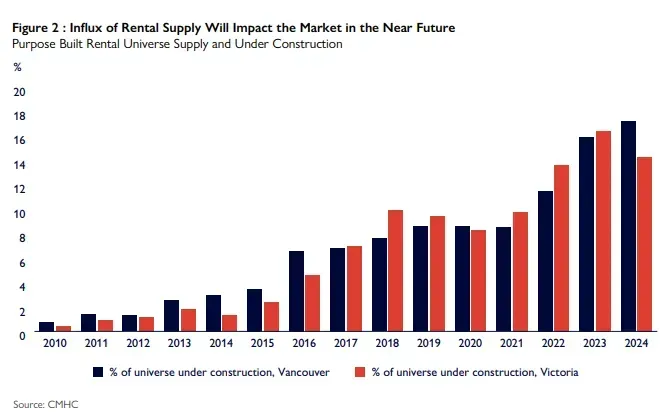

This chart shows that as of the end of 2024 in Vancouver, a whopping 17.2% of all purpose-built rental units in Vancouver were currently under construction. This is an all-time high figure, and will put downward pressure on rents as inventory comes online. The prospect of high land costs, high construction costs, regulatory and tax hurdles, lower immigration, and an influx of supply has developers looking elsewhere and to other asset types.

Our prediction: CMHC gets it right that housing starts are lower, but that they overestimate the number of new starts in each of 2025 and 2026. One potential caveat would be if the government dramatically reduces development fees, which would lower costs and give developers the confidence to proceed despite lower prospects for rent growth or appreciation.

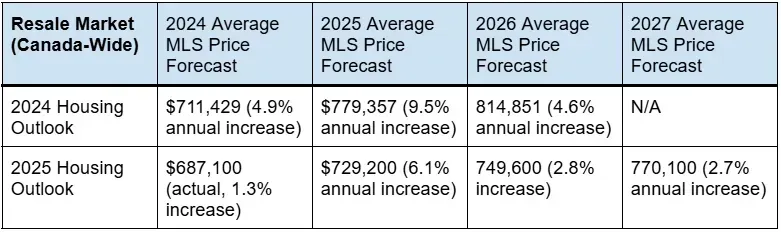

Home Prices Up

“We expect housing sales and prices to rebound as lower mortgage rates and changes to mortgage rules unlock pent-up demand in the short term. In the longer term, stronger economic fundamentals will support this rebound.”

CMHC's underlying thesis for higher resale prices is that the reduction in immigration demand will have less impact on housing than on rentals, and that lower mortgage rates will prop up housing prices.

It seems like an odd time to be projecting out ‘stronger economic fundamentals’ for 2026 and 2027, but maybe that’s just us?

Our prediction: We think that there is less pent-up demand in the market than what CMHC projects and that fears of economic downturn will prevent large housing price increases in 2025. We see it as unlikely that housing prices rise by the 6.1% forecast for 2025, but feel that their 2026 and 2027 price growth rates are more reasonable.

Rents Keep Climbing

“A record number of units are under construction as part of efforts to increase rental supply… As more new, higher-priced units come onto the market, average rents will continue rising. However, we expect asking rents to be negatively pressured as rental demand declines.”

In this report, CMHC doesn’t give Canada-wide rental forecasts, only regional forecasts. As such, we focus on the Vancouver rental market in this article.

CMHCs rationale for three years of ~6% rental price increases feels incredibly weak, even if they did adjust downward somewhat from their 2024 predictions. Yes, the wave of new units that come onto the market will be priced above current averages, and given the size of that wave, it will have a noticeable effect.

However, even before any economic weakness that stems from potential tariffs, demand is already falling and will continue to do so as plans to slow immigration kick in.

Our Prediction: CMHC is overestimating rental price increases, as they continue to underestimate the slowdown in demand and the cooling effect of new supply. In our view, we anticipate flat or low rental growth rates in Vancouver, and believe that negative rent rates are a real possibility over the next couple of years.

What does this mean for investors?

CMHC continues to paint an optimistic picture for investors in the BC housing market, but in our view, the data is leading us to believe a more bearish stance is prudent when underwriting.

At the least, investors will want to make sure that potential investments will still yield acceptable returns in a lower growth environment than what CMHC has projected.

In the meantime, we continue to look at deals on both sides of the border. While we believe many markets in Canada are in for some turbulence, we are more bullish on U.S. multifamily (see our last article), where a number markets are seeing new supply dwindle and rents are starting to grow again.